An Illustrated Tale of A.W. Phillips and his Eponymous Curve

A.W. Phillips led an interesting life. Born in New Zealand he left before finishing high school, worked as a crocodile hunter, and found himself in a country when the Japanese invaded not once, not twice, but three times! The last of these resulting in him spending three and a half years as a prisoner of war. But perhaps even more interesting than the life of A.W. Phillips is the life of his eponymous curve and it this life story which follows.

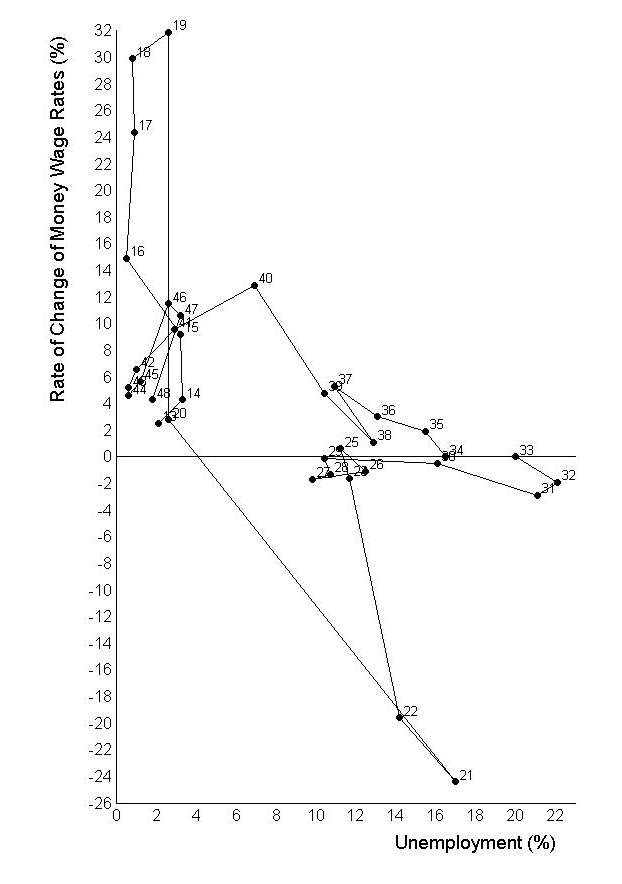

The Original Phillips Curve: Rate of Change of Wages against Unemployment, United Kingdom 1913 – 1948.

In 1958 William Phillips published his eponymous Phillips curve, showing a negative correlation between wage inflation and gross domestic product in the United Kingdom, 1913 – 1948. Similar results in other countries led many Economists during the 1960s —including the future Nobel winners Robert Solow and Paul Samuelson— to conclude that this negative correlation between inflation and unemployment was a deep relationship in the economy, and one that could be exploited. Interpreted as a structural relationship the Phillips curve suggested that a country could permanently lower it’s unemployment rate simply by putting up with a few percentage points more of inflation. This was an opportunity not to be missed!

A combination of stimulatory fiscal policy by the US Government, and expansionary monetary policy by the Federal Reserve Bank during the 1960s and 1970s was implemented do just this.1 The Federal Government ran a budget deficit that increased gradually from around zero in 1960 to 5 percent of GDP in the early 1980s.2 This combination of stimulatory fiscal and, especially, monetary policy achieved its first goal: increasing inflation. The US inflation rates went from an average of 1.3 percent for 1960-65, to a peak of around 14 percent in early 1980. So the first goal of increasing inflation to exploit the Phillips curve was attained. But the second goal of decreasing unemployment was not. Instead the Phillips curve fell apart!

Rather than increasing inflation leading to decreased unemployment as predicted based on the interpretation of the Phillips curve as a structural relationship, unemployment increased. This breakdown of the Phillips curve when exploited was not entirely unforeseen. Milton Friedman and Edmund Phelps, two Economists who would go on to win Nobels, had both warned that the Phillips curve was a mere correlation, and not a structural relationship that could be exploited. Friedman, in his 1968 Presidential address to the American Economics Association argued that the Phillips curve was simply as short-run phenomenon. The relationship was really between fluctuations in inflation and the unemployment rate. When inflation was deliberately increased to exploit this relationship people would simply adjust their expectations about inflation upwards. This would appear as an upward shift in the short-run Phillips curve. So the long-run Phillips curve could be thought of as a vertical line, with any average inflation level giving rise to the same unemployment rate. Also in 1968, Phelps published “Money-Wage Dynamics and Labor Market Equilibrium”, setting out a model of inflation and unemployment in which imperfect information gave rise to the short-run Phillips curve (short-run inflation was unexpected), while people’s ‘adaptive expectations’ meant that the short-run Phillips curve would gradually shift up in response to any increase in average (expected) inflation. The success of these predictions over the following decade demonstrated the importance of expectations, uncertainty, and dynamics in macroeconomic theory.3

The ‘Great Inflation’ of the United States found parallels in many other countries. In some, such as the United Kingdom, this occoured for much the same reasons, namely attempts to exploit the Phillips curve. In others inflation was ‘imported’ throughout the 1960s under the Bretton Woods international monetary system. Under Bretton Woods the US dollar was convertible to gold (i.e. pegged to gold), and other countries then pegged their currencies to the US dollar. To maintain their currencies at a fixed exchange rate with the US dollar meant that if the value of the US dollar fell due to US inflation, then other countries had to decrease the value of their currencies by inflation. In this way increasing US inflation lead to increasing inflation in other countries, even those not actively trying to exploit the Phillips curve. This situation continued until US President Nixon suspended the gold convertibility of the US dollar in 1971. This made the US dollar a fiat currency —destroying the Bretton Woods international monetary system— and a number of countries followed suit by floating their exchange rates. Not all other countries experience a great inflation, one particularly noteworthy exception being Germany; highly averse to inflation after its traumatic experience with hyperinflation in the early 1920s.

The end of the Great Inflation in the US came in the early 1980s following the appointment of Paul Volcker as Chairman of the Federal Reserve Bank in 1979, and the election of Ronald Reagan as US President in 1981. Under Volcker the Federal Reserve started tightening monetary policy towards the end of 1979, and began targeting the monetary base rather than the fed funds rate as the policy instrument. In late 1979 and early 1980 interest rates rose significantly. Then came a short recession in early 1980, accompanied by an increase in unemployment and an easing of inflation; the Federal Reserve —reacting in part to political pressure4— blinked and allowed the Fed Funds Rate to fall. The second half of 1980 saw an economic recovery, while inflation remained high. The Federal Reserve began to tighten again. The election of Reagan in January 1981 provided Volcker and the Federal Reserve with the political cover to continue with a tight monetary policy. The economy entered another recession in July 1981, more severe than the earlier one, and recovery did not begin until November 1982. By the time the recession ended inflation was down below 5 percent. But this came at a cost with the recession leading unemployment to peak at 11 percent. With inflation broken, the Federal Reserve eased off and the economic recovery of 1983 and 1984 was swift, with substantial growth in GDP and rapidly falling unemployment. Inflation remained low. The Great Inflation had ended.

The importance of inflation as a political issue in late 1970s US is easily overlooked today, but is shown strongly by the polls. “In a September 1979 survey, 67 percent of the public said that “holding down inflation” was a bigger problem than “finding jobs” (21 percent). On Election Day 59 percent of Reagan’s supporters said that inflation was a “determining issue for them,” according to the New York Times/CBS exit poll.” (R. Samuelson, 2010) While opposition to the Federal Reserves tight monetary polices came from many sources, Reagan was supportive in private meetings with Volcker. Attesting to the importance of the political cover Volcker has written: “No central bank can — or should, in my judgment — conduct policies for long that are out of keeping with basic, continuing objectives of the political system.”

In many other countries high inflation continued for a while longer. Australia for instance did not return to low inflation until after the recession of 1990. A recession described by then Treasurer Paul Keating as “The recession we had to have”.5 New Zealand returned to low inflation around the same time with the introduction of a policy of Inflation Targeting, innovative for its time and now standard for monetary policy in many countries.

In the world of Economic models and theory the success of the then new style of Macroeconomics which emphasized microfoundations and expectations, asserting that reduced-form relationships such as the Phillips Curve are misleading when thinking about the effects of economic policies, received a major boost based on the view that it not only explained but had correctly predicted the failure of attempts to exploit the Phillips curve. But that is a story for another time.

William “A.W.” Phillips

William Phillips was born in New Zealand in 1914. Unusually for an Economist he also had an interesting life. Here is a short version:

Alban William Housego Phillips was born at Te Rehunga near Dannevirke, New Zealand. As a young student he rebuilt the engine of a broken down car and (illegally) drove it to and from High School. He left New Zealand before finishing school to work in Australia at a variety of jobs, including crocodile hunter and manager of his own cinema. In 1937 Phillips headed to China, but had to escape to Russia when Japan invaded China. He traveled across Russia on the Trans-Siberian Railway and made his way to Britain in 1938, where he studied electrical engineering.

At the outbreak of World War II, Phillips joined the Royal Air Force and was sent to Singapore. When Singapore fell he escaped to Java, Indonesia. When Java, too, was overrun Phillips was captured by the Japanese, and spent three and a half years interned in a prisoner of war camp. During this period he learned Chinese from other prisoners, repaired and miniaturized a secret radio hidden in a clog, and fashioned a secret water boiler for tea which he hooked into the camp lighting system. In 1946, he was made a Member of the Order of the British Empire for his war service.

After the war he moved to London and began studying sociology at the London School of Economics (LSE), because of his fascination with prisoners of war’s ability to organize themselves. But he became bored with sociology and developed an interest in Keynesian theory, so he switched his course to economics and within eleven years was a professor of economics.

While a student at the LSE Phillips used his training as an engineer to develop MONIAC, an analogue computer which used hydraulics to model the workings of the British economy, inspiring the term hydraulic macroeconomics.6 It was very well received and Phillips was soon offered a teaching position at the LSE. He advanced from assistant lecturer in 1951 to professor in 1958.

His work focused on British data and observed that in years when the unemployment rate was high, wages tended to be stable, or possibly fall. Conversely, when unemployment was low, wages rose rapidly. In 1958 Phillips published his work on the relationship between inflation and unemployment, illustrated by the Phillips curve. He made several other notable contributions to economics, particularly relating to stabilization policy and Econometrics.

He returned to Australia in 1967 for a position at Australian National University which allowed him to devote half his time to Chinese studies. In 1969 the effects of his war deprivations and smoking caught up with him. He had a stroke, prompting an early retirement and return to Auckland, New Zealand, where he taught at the University of Auckland. He died in Auckland on 4 March 1975.

This bio is based on the Wikipedia article on his life, the Memoirs of his sister Carol Somervell, and Bollard article on his professional life.

Further reading:

The Great Inflation and Its Aftermath: The Past and Future of American Affluence, by Robert J. Samuelson: For those interested in reading more on the history of the Phillips curve and the Great Inflation, both political and its importance to the development of Macroeconomic theory. The book is US centric, but does discuss some of the international aspects.

Phillips (1958) – The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957.

Provides graph shown above. Also emphasizes that the same graph is stable across sub-periods of the time period he considers. Phillips was not the first to posit a relationship between prices and unemployment/output, but was the first to provide convincing empirical evidence.

Samuelson & Solow (1960) – Analytical Aspects of Anti-Inflation Policy

Describe Phillips curve as a “menu of choices”. They are aware that the curve can shift, although they emphasize shifts for non-monetary reasons (changing union power, employment legislation, etc.). That a permanent shift in inflation might shift the curve does receive a single mention, but only as one point in a lengthy laundry-list of possibilities, not as anything remotely likely to occour. They emphasize that the Phillips curve “menu of choices” should be viewed as something existing on a sub-five year timescale, but with the view that shifts will be due to changes in institutions/structure of economy, and that a slightly different menu of choices would then continue to exist.

Friedman (1968) – The Role of Monetary Policy (1968 Presidential Address to the American Economics Association)

Emphasizes expectations and that the ability of monetary policy to effect unemployment (and interest rates) is a short (sub-five year) phenomenon, with longer term unemployment and interest rates determined by real economic fundamentals.

Phelps (1967) – Phillips Curves, Expectations of Inflation and Optimal Unemployment over Time

Phelps (1968) – Money-Wage Dynamics and Labor-Market Equilibrium

Provide an explicit model/theoretical basis for why expectations matter and will shift the Phillips curve. From the perspective of Economic Theory these articles provide the basic framework by which the Phillips curve is understood today.

Footnotes:

1. The role of the Federal Reserve Bank was that of enabler. It did not deliberately aim to create inflation to exploit the Phillips curve (at least based on a reading of its minutes), instead it simply accommodated increasing inflation under the justification of the Phillips curve.

2. Another part of the justification for this was Keynesian counter-cyclical fiscal stimulus, but while the deficit is somewhat counter cyclical it never closed as much in the booms as it opened in the recessions. The growing trend in Government deficits makes sense under the goal of increasing inflation to exploit the Phillips curve. It makes no sense as counter-cyclical Keynesian fiscal policy.

3. Adaptive expectations has since largely disappeared from formal models, pushed out by rational expectations. It does still get some use however and also finds parallels in modern models in the form of learning under imperfect information (which is not a violation of rational expectations).

4. While Carter had recognized the failure of voluntary and involuntary price and wage controls and appointed Volcker to fight inflation Miller and Schultze, Carter’s Treasury Secretary and chairman of the Council of Economic Advisors respectively, both opposed the actions of the Federal Reserve.

5. While the Reserve Bank of Australia was running a tight monetary policy at the time of the 1990 recession, unlike in the US case of 1980 and 1981-82 recessions this was not viewed as a recession induced by the central bank to fight inflation.

6. MONIAC, Monetary National Income Analogue Computer, is a small open-economy ISLM model with a financial accelerator. Videos of a MONIAC in action can be found online, as can a simulated version with explanation. The MONIAC draws graphs that Economists would recognize as the transition paths between steady-states. A few MONIACs remain in existence, with the only regularly working one located at the Reserve Bank of New Zealand where it can be seen in action once a month. The precise mathematical model solved by the MONIAC consists of nine differential equations, see Phillips (1950) – Mechanical Models in Economic Dynamics. The only other working MONIAC is located in Cambridge, UK and is run once per year.

Comments are Disabled